PART I INTRODUCTION TO COST MANAGEMENT C H A P T E R F I V E Activity-Based Costing and Management After studying this chapter, you should be able to . . . Explain the strategic role of activity-based costing Describe activity-based costing (ABC), the steps in developing an ABC system, and the benefits and limitations of an ABC system Determine product costs under both the volume-based method and the activity-based method and contrast the two Explain activity-based management (ABM) Describe how ABC/M is used in manufacturing companies, service companies, and governmental organizations Use an activity-based approach to analyze customer profitability Identify key factors for successful ABC/M implementation Beware of little expenses. A small leak will sink a great ship. Benjamin Franklin This chapter has a lot to do with implementing the spirit of Benjamin Franklin’s observa- tion—in cost management terms—that it really does matter how accurately you calculate a cost. Why? Having accurate costs is important for a variety of reasons: a company might find that it has a difficult time determining which of its products is most profitable. Alterna- tively, it finds its sales increasing but profits declining and cannot understand why. Perhaps the company keeps losing competitive bids for products and services and does not understand why. In many cases, accurate cost information is the answer to these questions. Accurate cost information provides a competitive advantage. It helps a company or organization to develop and to execute its strategy by providing accurate information about the cost of its products and services, the cost of serving its customers, the cost of dealing with its suppliers, and the cost of supporting business processes within the company. 1. 2. 3. 4. 5. 6. 7. 120 Activity-based costing (ABC) is a method for determining accurate costs. While ABC is a relatively recent innovation in cost accounting, it is rapidly being adopted by companies across many industries and within government and not-for-profit organizations. Here is a quick ex- ample of how it works, and why it is important Suppose you and two friends (Joe and Al) have gone out for dinner to have pizza. You each order an individual size pizza, and Al suggests that you all order a plate of appetizers for the table. You and Joe figure you will have a bite or two of the appetizers, so you say OK. Dinner is great, but at the end Al is still hungry, so he orders another plate of appetizers and as before, eats all of it. When it is time for the check, Al sug- gests the three of you split the cost of the meal equally. Is this fair? Perhaps Al should offer to pay for the two appetizer plates. The individual pizzas are direct costs for each of you so that an equal share is fair, but while the appetizer plate was intended to be shared equally, it turns out that Al consumed most of it. LEARNING OBJECTIVE 1 Explain the strategic role of activity-based costing LEARNING OBJECTIVE 1 Explain the strategic role of activity-based costing The Strategic Role of Activity-Based Costing blo28155_ch05.indd 120 blo28155_ch05.indd 120 5/17/06 6:19:47 PM 5/17/06 6:19:47 PM

Transcript

PART

I IN

TRO

DU

CTIO

N T

O C

OST

MAN

AGEM

ENT

C H A P T E R F I V E

Activity-Based Costing and Management After studying this chapter, you should be able to . . .

Explain the strategic role of activity-based costing

Describe activity-based costing (ABC), the steps in developing an ABC system, and the benefi ts and limitations of an ABC system

Determine product costs under both the volume-based method and the activity-based method and contrast the two

Explain activity-based management (ABM)

Describe how ABC/M is used in manufacturing companies, service companies, and governmental organizations

Use an activity-based approach to analyze customer profi tability

Identify key factors for successful ABC/M implementation

Beware of little expenses. A small leak will sink a great ship.

Benjamin Franklin

This chapter has a lot to do with implementing the spirit of Benjamin Franklin’s observa-tion—in cost management terms—that it really does matter how accurately you calculate a cost. Why? Having accurate costs is important for a variety of reasons: a company might fi nd that it has a diffi cult time determining which of its products is most profi table. Alterna-tively, it fi nds its sales increasing but profi ts declining and cannot understand why. Perhaps the company keeps losing competitive bids for products and services and does not understand why. In many cases, accurate cost information is the answer to these questions. Accurate cost information provides a competitive advantage. It helps a company or organization to develop and to execute its strategy by providing accurate information about the cost of its products and services, the cost of serving its customers, the cost of dealing with its suppliers, and the cost of supporting business processes within the company.

1.

2.

3.

4.

5.

6.

7.

120

Activity-based costing (ABC) is a method for determining accurate costs. While ABC is a relatively recent innovation in cost accounting, it is rapidly being adopted by companies across many industries and within government and not-for-profi t organizations. Here is a quick ex-ample of how it works, and why it is important Suppose you and two friends (Joe and Al) have gone out for dinner to have pizza. You each order an individual size pizza, and Al suggests that you all order a plate of appetizers for the table. You and Joe fi gure you will have a bite or two of the appetizers, so you say OK. Dinner is great, but at the end Al is still hungry, so he orders another plate of appetizers and as before, eats all of it. When it is time for the check, Al sug-gests the three of you split the cost of the meal equally. Is this fair? Perhaps Al should offer to pay for the two appetizer plates. The individual pizzas are direct costs for each of you so that an equal share is fair, but while the appetizer plate was intended to be shared equally, it turns out that Al consumed most of it.

LEARNING OBJECTIVE 1 Explain the strategic role of activity-based costing

LEARNING OBJECTIVE 1 Explain the strategic role of activity-based costing

Chapter 5 Activity-Based Costing and Management 121

There are similar examples in manufacturing. Suppose you and Joe and Al are also product managers at a plant that manufactures furniture. Al is in charge of sofa manufacturing, Joe of dining room tables and chairs, and you are in charge of bedroom furniture. Each of your product lines has direct materials and labor costs that are traced directly to each of you. It is your responsibility to manage these direct costs. Also, there are indirect manufacturing costs (overhead) that cannot be traced to each product, including, the following activities: materials acquisition, materials storage and handling, product inspection, manufacturing supervision, job scheduling, equipment maintenance, and fabric cutting. What if the company decides to charge each of the three product managers a “fair share” of the total indirect cost using the ratio of units produced in a manager’s area to the total units produced for all managers? This approach is described in Chapter 4 and is commonly referred to as volume-based costing . Note that whether the proportions used are based on units of product, direct labor hours, or machine hours, each of these is volume-based.

But if, as is usually the case, the usage of these activities is not proportional to the number of units produced, then some managers will be overcharged and others undercharged under the volume-based approach. For example, suppose Al insists on more frequent inspections of his production; then he should be fairly charged a higher proportion of overhead (inspection) than that based on units alone. Moreover, why should you pay any portion of fabric cutting if your bedroom furniture does not require fabric?

Another consideration is that the volume-based method provides little incentive for the manager to control indirect costs. Unfortunately, the only way you could reduce your share of the indirect costs is to reduce your units produced (or hope that Joe and/or Al increase production)—not much of an incentive. On refl ection, the approach that charges indirect costs to product based on units produced does not provide very accurate product cost for you or Joe or Al and certainly does not provide the appropriate incentives for managing the indirect costs. The solution is to use activity-based costing to charge these indirect costs to the products, using detailed information on the activities that make up the indirect costs—the materials handling, inspection, fabric cutting, and materials handling. This chapter shows how to do it.

A good example of one of many success stories for ABC is the application of ABC at the U.S. Postal Service (USPS). The ABC application at USPS originated from the Postmaster General’s directive to develop a costing system that would help the USPS to become more competitive and to serve as a basis for comparing performance among the various mail-processing facilities. The initial ABC system used 58 work activities and nine cost objects. The cost objects included handling of letters, fl ats, small parcels, large parcels, priority mail, express mail, registered mail, large mail containers, and small mail containers. In the initial application at a single mail-processing facility, there was a reduction of 13% in total cost as a result of the improved understanding of cost behavior in the facility. The USPS also used ABC to determine the cost differences in processing payments from customers who used cash, checks, or credit cards and from this analysis determined that the low-cost approach was to use credit cards. The ABC-based analyses have helped the USPS to implement an effective, cost-competitive strategy.

Volume-based costing can be a strategic good choice for some fi rms. It is appropriate gener-ally when direct costs are the major cost of the product or service and activities supporting the production of the product or service are relatively simple, low-cost, and homogenous across different product lines. This may be the case, for example, for a commodity manufacturer that has one or a few very homogeneous product lines—for example, a fi rm that manufactures paper products or a fi rm that produces certain agricultural products. Similarly, a professional service fi rm (law fi rm, accounting fi rm) may not need ABC because labor costs for the pro-fessional staff are the largest cost of the fi rm, and labor is also easily traced to clients (the cost object). For fi rms other than these, the ABC approach is often preferred: the volume-based approach will cause signifi cant inaccuracies in the product costs—some products will be overcosted and others undercosted because the usage of activities is not in proportion to the volume of output.

To develop a costing system we need to understand relationships among resources, activities, and products or services. Resources are spent on activities and products or services are a result of activities. Many of the resources used in an operation can be traced to individual products or services and identifi ed as direct materials or direct labor costs. Most overhead costs relate only indirectly to fi nal products or services. Nevertheless, overhead costs are resources spent on a fi rm’s activities to manufacture products, provide services, or facilitate manufacturing. A good costing system identifi es costs with activities that consume resources and assign re-source costs to cost objects such as products, services, or intermediate cost pools based on activities performed for the cost objects.

Resources, Activities, Resource Consumption Cost Drivers, and Activity Consumption Cost Drivers Before discussing activity-based costing, we need to defi ne several important terms: activity, resource, cost driver, resource consumption cost driver, and activity consumption cost driver.

An activity is a specifi c task or action of work done. An activity can be a single action or an aggregation of several actions. For example, moving inventory from workstation A to worksta-tion B is an activity that may require only one action. Production set-up is an activity that may include several actions.

A resource is an economic element needed or consumed in performing activities. Sala-ries and supplies, for example, are resources needed or used in performing manufacturing activities.

A cost driver is a factor that causes or relates to a change in the cost of an activity. Because cost drivers cause or relate to cost changes, measured or quantifi ed amounts of cost drivers are excellent bases for assigning resource costs to activities and for assigning the cost of activities to cost objects.

A cost driver is either a resource consumption cost driver or an activity consumption cost driver . A resource consumption cost driver is a measure of the amount of resources consumed by an activity. It is the cost driver for assigning a resource cost consumed by or related to an activity to a particular activity or cost pool. Examples of resource consumption cost drivers are the number of items in a purchase or sales order, changes in product design, size of factory buildings, and machine hours.

An activity consumption cost driver measures the amount of an activity performed for a cost object. It is used to assign activity cost pool costs to cost objects. Examples of activity consumption cost drivers are the number of machine hours in the manufacturing of product X, or the number of batches used to manufacture Product Y.

What Is Activity-Based Costing? Activity-based costing (ABC) is a costing approach that assigns resource costs to cost objects such as products, services, or customers based on activities performed for the cost objects. The premise of this costing approach is that a fi rm’s products or services are the results of activities and activities use resources which incur costs. Costs of resources are assigned to activities based on the activities that use or consume resources (resource consumption driv-ers), and costs of activities are assigned to cost objects based on activities performed for the cost objects (activity consumption drivers). ABC recognizes the causal or direct relationships between resource costs, cost drivers, activities, and cost objects in assigning costs to activities and then to cost objects.

ABC assigns factory overhead costs to cost objects such as products or services by identifying the resources and activities as well as their costs and amounts needed to produce output. Using resource consumption cost drivers, a fi rm determines the resource costs consumed by activities or activity centers (activity cost pools) and calculates the cost of a unit of activity. The fi rm then assigns the cost of an activity to products or services by multiplying the cost of each activity by the amount of the activity consumed by each of the cost objects.

LEARNING OBJECTIVE 2 Describe activity-based costing (ABC), the steps in developing an ABC system, and the benefi ts and limitations of an ABC system

LEARNING OBJECTIVE 2 Describe activity-based costing (ABC), the steps in developing an ABC system, and the benefi ts and limitations of an ABC system

An activity is a specifi c task or action of work done.

An activity is a specifi c task or action of work done.

A resource is an economic element needed or consumed in performing activities.

A resource is an economic element needed or consumed in performing activities.

A resource consumption cost driver is an activity or characteristic that consumes resources.

A resource consumption cost driver is an activity or characteristic that consumes resources.

An activity consumption cost driver measures how much of an activity a cost object uses.

An activity consumption cost driver measures how much of an activity a cost object uses.

Activity-based costing (ABC) is a costing approach that assigns resource costs to a cost object based on activities performed for the cost object.

Activity-based costing (ABC) is a costing approach that assigns resource costs to a cost object based on activities performed for the cost object.

Chapter 5 Activity-Based Costing and Management 123

The Two-Stage Cost Assignment Procedure A two-stage cost assignment procedure assigns resource costs such as factory overhead costs to activity cost pools and then to cost objects to determine the amount of resource costs for each of the cost objects. Volume-based costing systems assign factory overhead costs fi rst to plant or departmental cost pools and second to products or services (see Exhibit 5.1 ). Volume-based systems, in the fi rst stage, charge factory overhead costs to a single plant cost pool or to departmental cost pools. This approach is convenient and simple, because many accounting systems in use today accumulate cost information by department, which is easily aggregated to the plant level. In the second stage, a volume-based rate (based on units produced or hours used in production) is then used to apply overhead to each of the cost objects. The volume-based approach is used in Chapter 4 in job costing. A volume-based two-stage cost assignment procedure, however, is likely to distort product or service costs. This is true especially in the second stage where the volume-based costing system uses a cost driver such as direct labor-hours or output units to assign factory overhead costs. Because all products or services do not always consume factory overhead resources in a cost pool in proportion to the volume-based measure or measures the fi rm uses to assign factory overhead costs, a volume-based system often leads to inaccurate measures for the costs of support activities in its operations. This distortion becomes more serious especially when a substantial portion of factory overhead costs is not output-volume related and the fi rm manufactures a diverse mix of products with differences in volumes, sizes, or complexities.

Activity-based costing systems differ from volume-based costing systems by tracing uses of resources to activities and linking activity costs to products, services, or customers (see Exhibit 5.2 ). The fi rststage assigns factory overhead costs to activities or activity cost centers (activity cost pools) by using appropriate resource consumption cost drivers. The secondstage assigns the costs of activities or activity cost pools to cost objects using appropriate activity consumption cost drivers that measure the demands cost objects place on the activities. By using cost drivers in both the fi rst and second stage cost assignments, activity-based costing systems provide more accurate measures of product or service costs for the cost of activities that are not proportional to the volume of outputs produced.

In summary, activity-based costing systems differ from volume-based costing systems in two ways. First, the ABC system defi nes cost pools as activities rather than production plant or department cost centers. Second, the cost drivers that the ABC system uses to assign acti-vity costs to cost objects are drivers based on an activity or activities performed for the cost object. The volume-based approach uses a volume-based cost driver that often bears little or no relationship to the consumption of resource cost by the cost objects.

A two-stage cost assignment assigns factory overhead costs to activity cost pools and then to cost objects.

A two-stage cost assignment assigns factory overhead costs to activity cost pools and then to cost objects.

Resources

Direct Materialsand Direct Labor

Indirect Costs(Overhead)

Cost Objects

Second Stage: Activitycost pools assigned tocost objects usingactivity consumptioncost drivers

First Stage: Direct materialsand labor assigned to costobjects; overhead costsassigned to activities usingresource consumptioncost drivers Cost Pools: The

activities in theplant

EXHIBIT 5.2 The Activity-Based Two-Stage Procedure

Resources

Direct Materialsand Direct Labor

Indirect Costs(Overhead)

Cost Pools: Theplant or thedepartments in theplant

Cost Objects

Second Stage: Plantlevel or departmentalcosts assigned to costobjects using volume-based cost drivers

First Stage: Directmaterials and laborassigned to cost objects;overhead costs assignedto department directly oraggregated to plant level

Developing an activity-based costing system entails three steps: (1) identifying resource costs and activities, (2) assigning resource costs to activities, and (3) assigning activity costs to cost objects. Steps one and two constitute stage 1 from Exhibits 5.1 and 5.2 , and Step 3 is equiva-lent to stage 2 from these exhibits.

Step 1: Identify Resource Costs and Activities The fi rst step in designing an ABC system is to conduct an activity analysis to identify the resource costs and activities of the fi rm. Most fi rms record resource costs in specifi c ac-counts in the accounting system. Examples of these accounts include supplies, purchasing, materials handling, warehousing, offi ce expenses, furniture and fi xtures, buildings, equip-ment, utilities, and salaries and benefi ts. However, special effort most likely will be needed to determine appropriate resource costs for activity-based costing because generally several different resource costs may be recorded in a single account or the costs for an activity may be recorded in several accounts. For example, a fi rm may use a single factory supplies ac-count for all supplies in its operations that include several manufacturing operations. Costs to complete a purchasing order may be spread over several accounts including accounts for warehousing, purchasing, and receiving.

Through activity analyses a fi rm identifi es the work it performs to carry out its operations. Activity analyses include gathering data from existing documents and records, as well as collecting additional data using questionnaires, observations, or interviews of key personnel. Questions that ABC project team members typically ask employees or managers in gathering activity data include:

• What work or activities do you do?

• How much time do you spend performing these activities?

• What resources are required to perform these activities?

• What value does the activity have for the product, service, customer, or organization?

With the help of industrial engineers and management accountants, the team also collects activity data by observing the work performed and making a list of all the activities involved.

Levels of Activities

To identify resource costs for various activities, a fi rm classifi es all activities according to the way in which the activities consume resources.

A unit-level activity is performed on each individual unit of product or service of the fi rm. Examples of unit-level activities include direct materials, direct labor-hours, inserting a

1. A unit-level activity is performed for each unit of the cost object.

A unit-level activity is performed for each unit of the cost object.

REAL-WORLD FOCUS Traditional Costing System Distorted Product Costs at Xi’an Electronics in China

Xi’an Electronics produces special electronics with more than 250 products that have in excess of 600 specifi cations. Researchers col-lected data for 25 of the company’s products during the last half of 1997 and grouped them into two product categories, high volume and low volume. They found that the unit conversion cost (direct labor and overhead) was 29.58 percent higher under traditional costing (using direct labor hours as the cost driver) than ABC (using 30 cost drivers)

for high-volume products and was 45.95 percent lower under tradi-tional costing than ABC for low-volume products. Their fi ndings show that traditional costing overestimates the costs of high-volume prod-ucts and underestimates the costs of low-volume products.

Source: Pingxin Wang, Qinglu Jin, and Dagang Ke, “Activity-Based Costing and Its Application in Chinese Enterprises,” China Accounting and Finance Review, March 2000, pp. 138–55.

The two-stage allocation procedure in an activity-based costing system identifi es clearly the costs of activities of a fi rm. The assignment of activity costs to cost objects uses a measure or measures that represent the demands the cost objects make on activities of the fi rm. As a result, activity-based costing systems report more accurate product or service costs than tradi-tional volume-based costing systems do.

Steps in Developing an Activity-Based Costing System

Chapter 5 Activity-Based Costing and Management 125

component, and inspecting every unit. A unit-level activity is volume-based. The required activity varies in proportion with the quantity of the cost object. The resource consump-tion driver and the activity consumption driver are most likely to be the same for unit level activities.

A batch-level activity is performed for each batch or group of units of products or services. A fi rm incurs a batch-level activity for each batch or group of units of products or services scheduled to be processed together, rather than for each individual unit of the cost object. A batch has more than one unit of a product or service. Examples of batch-level activities are setting up machines, placing purchase orders, scheduling production, conducting inspec-tions by batch, handling materials, and expediting production.

A product-level activity supports the production of a specifi c product or service. Examples of product-sustaining activities include designing products, administering parts required for products, and engaging in engineering changes to modify products.

A facility-level activity supports operations in general. These activities are not caused by products or customer service needs and cannot be traced to individual units, batches, or products. Examples of facility sustaining activities include providing security and safety, performing maintenance of general purpose machines, managing the plant, incurring fac-tory property taxes and insurance and closing of the books each month. Some fi rms refer to these activities as business or infrastructure sustaining activities.

Note that a unit-level activity can always be traced to a batch (one of the units in the batch), and a batch-level activity can always be traced to a product (one batch of this particular prod-uct), and a product-level activity can always be traced to a manufacturing facility; but, the reverse is not possible. Exhibit 5.3 illustrates activity level classifi cations at Siemens Electric Motor Works.

Step 2: Assign Resource Costs to Activities Activity-based costing uses resource consumption cost drivers to assign resource costs to activities. Because activities drive the cost of resources used in operations, a fi rm should choose resource consumption cost drivers based on cause-and-effect relationships. Typical resource consumption cost drivers include the number of (1) labor hours for labor intensive activities; (2) employees for payroll-related activities; (3) setups for batch-related activities; (4) moves for materials-handling activities; (5) machine-hours for machine repair and mainte-nance; and (6) square feet for general maintenance and cleaning activities.

Although a fi rm’s accounting system is a good starting point to fi nd information about the cost of resources, most accounting systems report the costs of different resources, such as indirect labor, electricity, equipment, and supplies, but do not report the cost of activi-ties performed. New accounting systems are needed to obtain and track resource costs for activities.

The cost of the resources can be assigned to activities by direct tracing or estimation. Direct tracing requires measuring the actual usage of resources by activities. For example, power used to operate a machine can be traced directly to that machine‘s operation by reading the meter attached to the machine.

When direct tracing is not available, department managers and supervisors need to estimate the amount or percentage of time (or effort) employees spend on each identifi ed activity.

Multiple resource consumption cost drivers often are needed to assign different resource costs to activity or activity center cost pools. Exhibit 5.4 illustrates resources and resources consumption drivers for factory overhead costs at AT&T’s New River Valley plant.

2.

3.

4.

A batch-level activity is performed for each batch or group of products or services.

A batch-level activity is performed for each batch or group of products or services.

A product-level activity supports the production of a specifi c product or service.

A product-level activity supports the production of a specifi c product or service.

A facility-level activity supports the operation in general.

A facility-level activity supports the operation in general.

Activity Activity Level

Direct materials UnitDirect labor-hours UnitMachine-hours UnitNumber of production orders BatchNumber of special components Batch

EXHIBIT 5.3Activities and Activity Levels at Siemens Electric Motor Works

Step 3: Assign Activity Costs to Cost Objects The fi nal step is to assign costs of activities or activity cost pools to cost objects based on the appropriate activity consumption cost drivers. Outputs are the cost objects for which fi rms or organizations perform activities. Typical outputs for a cost system are products and services; however, outputs also can include customers, projects, or business units. For example, the outputs of an insurance company may be individual insurance policies sold to customers, claims processed, types of policies offered, insurance agents, or divisions or subunits of the company.

Firms use activity consumption cost drivers to assign activity costs to cost objects. Acti-vity cost drivers should explain why the cost of a cost object goes up or down. Typical activity consumption cost drivers are purchase orders, receiving reports, inspection reports or hours, parts stored, payments, direct labor-hours, machine-hours, and setups and manufacturing cycle time. Careful analyses should be conducted in determining proper activity consumption cost drivers. For example, at the Hewlett-Packard (HP)’s Surface Mount Center in Boise, the ABC system has been fully operational since the early 1990s. This facility manufactures about 50 electronic circuit boards for internal HP customers. The center’s accounting, production, and engineering staffs jointly conducted an intense analysis of the production process and cost behavior patterns to select cost drivers. This combination of accounting and engineering analysis helped management choose cost drivers.

Since the 1980s an increasing number of fi rms have adopted the activity-based costing system. These fi rms adopt ABC because of the benefi ts it offers.

Benefi ts Initially, many fi rms adopt activity-based costing to reduce distortions in product costs often found in their volume-based costing systems. Volume-based costing systems, generate pro-duct or service costs bearing little or no relationship to activities and resources consumed in operations. ABC clearly shows the effect of differences in activities and changes in products or services on costs. Among the major benefi ts of activity-based costing that many fi rms have experienced are:

Better profi tability measures. ABC provides more accurate and informative product costs, leading to more accurate product and customer profi tability measurements and to better-informed strategic decisions about pricing, product lines, and market segments.

Better decision making. ABC provides more accurate measurements of activity-driving costs, helping managers to improve product and process value by making better product design decisions, better customer support decisions, and fostering value enhancement projects.

Process improvement. The ABC system provides the information to identify areas where process improvement is needed.

1.

2.

3.

Benefi ts and Limitations of Activity-Based Costing

Resource Resource Consumption Cost Driver

Personnel Number of workersStoreroom Number of items picked for an orderEngineers Time workedMaterials management Time workedAccounting Time workedResearch and development Number of new codes developedQuality Time workedUtilities Square-footage

EXHIBIT 5.4Resource and Resource Consumption Cost Drivers at AT&T’s New River Valley Plant

Cost estimation. Improved product costs lead to better estimates of job costs for pricing decisions, budgeting, and planning.

Cost of unused capacity. Since many fi rms have seasonal and cyclical fl uctuations in sales and production, there are times when plant capacity is unused. This can mean that costs are incurred at the batch-, product-, and facility-level activities but are not used . Capacity is supplied but not used in production ABC systems provide better information to identify the cost of unused capacity and maintain a separate accounting for this cost. For example, if a particular customer’s order requires the addition of a certain type of capacity in the plant, then the customer can be charged for that additional capacity. Alternatively, if a plant manager decides to add capacity in expectation of future increases in sales and production, then the cost of that additional capacity should not be charged to current production but charged as a lump sum in the plant’s costs. Overall, the goal is to manage capacity levels to reduce the cost of underutilization of capacity and to price products and services properly.

Limitations Although activity-based costing provides better product or service costs than volume based systems, managers should be aware of its limitations:

Allocations. Not all costs have appropriate or unambiguous activity or resource consump-tion cost drivers. Some costs require allocations to departments and products based on arbitrary volume measures because fi nding the activity that causes the cost is impractical. Examples are facility-sustaining costs such as the costs of the information system, factory manager’s salary, factory insurance, and property taxes for the factory.

Omission of costs. Product or service costs identifi ed by an ABC system are likely to not include all costs associated with the product or service. Product or service costs typically do not include costs for such activities as marketing, advertising, research and develop-ment, and product engineering even though some of these costs can be traced to individual products or services. Product costs do not include these costs because generally accepted accounting principles (GAAP) for fi nancial reporting require them to be treated as period costs.

Expense and time. An ABC system is not cost free and is time-consuming to develop and implement. For fi rms or organizations that have been using a traditional volume-based costing system, installing a new ABC system is likely to be very expensive. Furthermore, like most innovative management or accounting systems, ABC usually requires a year or longer for successful development and implementation.

4.

5.

1.

2.

3.

REAL-WORLD FOCUS Who Uses ABC and Why?

A 2001 survey of 166 users of ABC costing reported that most adopters used ABC to improve product costing, to assist in cost reduction, and to better assess the profi tability of its products and customers. Other common uses were for process improvement, cost estimation, pric-ing, and performance measurement. Many of the surveyed fi rms are in the manufacturing industry, and ABC was critical in fi nding compe-tition responses to industry price competition, identifying unprofi table products, and identifying unprofi table customers.

The survey also reported a signifi cant diversity among these fi rms in the number of activities, cost objects, and cost drivers. While some fi rms had several thousand activities in their ABC system, the majority had between 25 and 250. Also, while some fi rms had several thousand cost objects, most had fewer than 100. The most common number of resource and activity cost drivers was occasionally over 100 but for most fi rms was between 6 and 10.

A 2005 survey of the members of BetterManagement.com vali-dated these results. Drawn from 528 responses from the fi nancial services industry, manufacturing, and communications and public service sectors, the survey found that improved product costing, bet-ter analysis of both product and customer profi tability, and process improvement were the key goals of the ABC system. The usage of ABC was comparable across industries, though the manufacturing and fi nancial services industries placed more emphasis on product and customer profi tability, while in the public sector the key emphasis was on product costing and process improvement.

Source: Dan Swenson and Douglas Barney, “ABC/M: Which Companies Have Success?” The Journal of Corporate Accounting and Finance, March/April 2001, pp. 35–44.BetterManagement.com provides online resources for performance manage-ment (http://www.bettermanagement.com/). It is a wholly owned subsidiary of SAS Institute, Inc.

The following example contrasts Steps 2 and 3 of the volume-based costing system using direct labor-hours as the cost driver with an activity-based costing system that uses both volume-based and activity-based cost drivers.

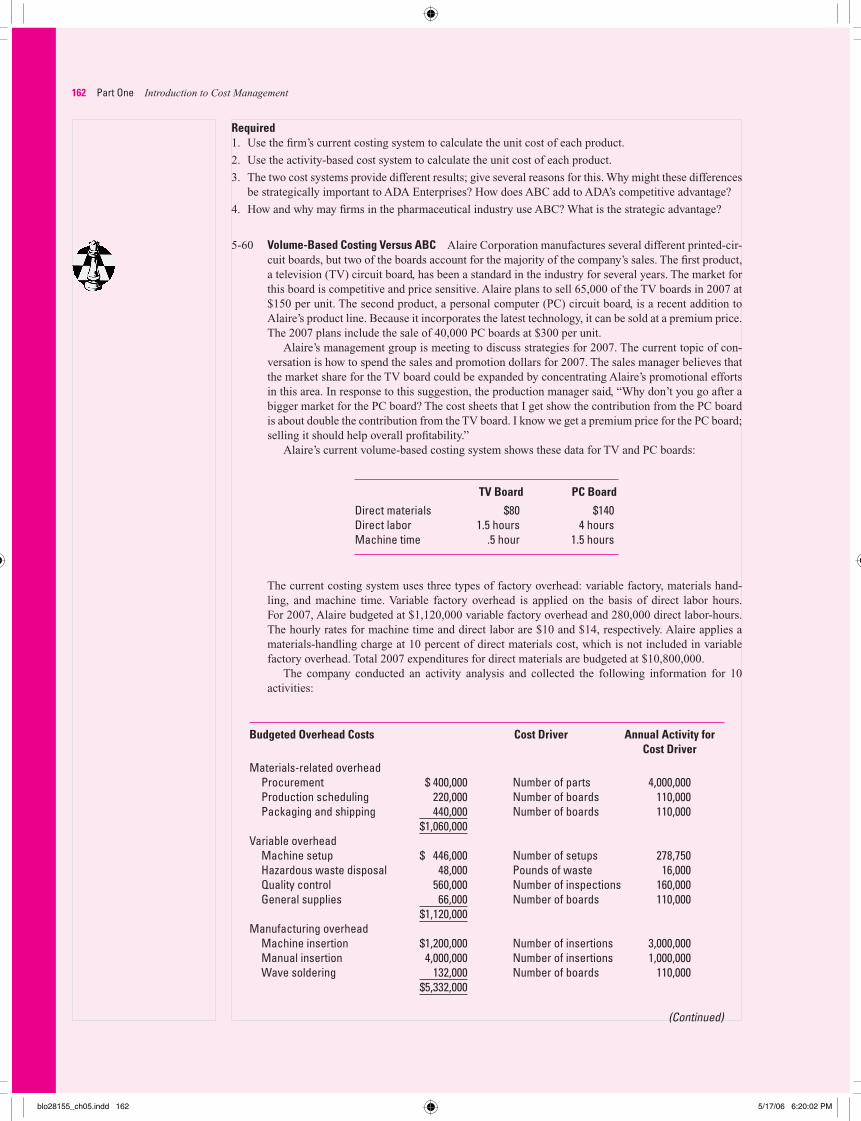

Haymarket BioTech, Inc. (HBT) produces and sells two secure communication systems, AW (Anywhere) and SZ (SecureZone). AW uses satellite technology and allows parties whose DNA is implanted in the device to communicate anywhere on the earth. SZ uses similar tech-nology except it allows communication between two parties who are within 10 miles of each other. HBT has the following operating data for the two products:

AW SZ

Production volume 5,000 20,000 Selling price $400.00 $200.00 Unit direct materials and labor $200.00 $ 80.00 Direct labor-hours 25,000 75,000 Direct labor-hours per unit 5 3.75

Volume-Based Costing The volume-based costing system that the fi rm uses assigns factory overhead (OH) based on direct labor-hours (DLH). The fi rm has a total budgeted overhead of $2,000,000. Since the fi rm budgeted 100,000 direct labor hours for the year, the overhead rate per direct labor hour is $20 per direct labor hour.

Total overhead $2,000,000 Total DLH 25,000 + 75,000 = 100,000 Overhead rate per DLH $ 20.00

Since the fi rm uses 25,000 direct labor hours to manufacture 5,000 units of AW, the factory overhead assigned to AW is $500,000 in total and $100 per unit:

Total OH assigned to AW $20 × 25,000 = $500,000 Number of units of AW 5,000 Factory overhead per unit of AW $ 100.00

The factory overhead for SZ is $1,500,000 in total and $75 per unit since the fi rm spent 75,000 direct labor hours to manufacture 20,000 units of SZ:

Total OH assigned to SZ $20 × 75,000 = $1,500,000 Number of units of SZ 20,000 Factory overhead per unit of SZ $ 75.00

In Exhibit 5.5 we show a product profi tability analysis using the fi rm’s volume based costing system.

LEARNING OBJECTIVE 3 Determine product costs under both the volume-based and the activity-based methods, and contrast the two

LEARNING OBJECTIVE 3 Determine product costs under both the volume-based and the activity-based methods, and contrast the two

A Comparison of Volume-Based and Activity-Based Costing

AW SZ

Unit selling price $400 $200Unit product cost:Direct materials and labor $200 $80Factory overhead 100 75Cost per unit 300 155 Unit margin $100 $ 45

EXHIBIT 5.5Product Profi tability Analysis under Volume-Based Costing

Chapter 5 Activity-Based Costing and Management 129

Activity-Based Costing In using an activity-based costing, HBT has identifi ed the following activities, budgeted costs, and activity consumption cost drivers:

Engineering $ 125,000 Engineering hours Setups 300,000 Number of setups Machine running 1,500,000 Machine-hours Packing 75,000 Number of packing orders Total $2,000,000

HBT also has gathered the following operating data pertaining to each of its products:

AW SZ Total

Engineering hours 5,000 7,500 12,500 Number of setups 200 100 300 Machine-hours 50,000 100,000 150,000 Number of packing orders 5,000 10,000 15,000

Using the gathered data, the cost driver rate for each activity consumption cost driver is calculated as follows:

Benefi ts of activity-based costing systems are not limited to improving product costings. After having an activity-based costing system in place, management often discovers that informa-tion from a well-designed ABC system helps to increase both the value customers received and the profi ts to the fi rm, especially for fi rms that embrace activity-based management.

What Is Activity-Based Management? Activity-Based Management (ABM) manages activities to improve the value of products or services to customers and increase the fi rm’s competitiveness and profi tability. ABM draws on ABC as its major source of information and focuses on the effi ciency and effectiveness of key business processes and activities. Using ABM, management can pinpoint avenues for impro-ving operations, reducing costs, or increasing values to customers. By identifying resources spent on customers, products, and activities, ABM improves management’s focus on the fi rm’s critical success factors and enhances its competitive advantage.

ABM applications can be classifi ed into two categories: operational ABM and strategic ABM. Operational ABM enhances operation effi ciency and asset utilization and lowers costs; its focuses are on doing things right and performing activities more effi ciently. Operational

Exhibit 5.6 presents a product profi tability analysis under the activity-based costing system and Exhibit 5.7 compares product costs and profi t margins under the two costing systems.

Remember that one major limitation of a volume-based costing system is that it tends to undercost complex low-volume products and overcost high-volume products. The activity-based costing system presents a more accurate measurement of product costs by tracing over-head consumption. The preceding comparison shows that the volume-based product costing system signifi cantly undercosts AW (a low-volume product) and overcosts SZ (a high-volume product) when considering the actual overhead consumptions of the two products. This is sometimes called cross-subsidization , that is, the cost accounting subsidizes some products at the expense of others. Distorted or inaccurate product costing can lead to inappropriate inven-tory valuations, unrealistic pricing, ineffective resource allocations, misplaced strategic focus, misidentifi ed critical success factors, and lost competitive advantage.

Activity-Based Management

AW SZ

Unit selling price $400 $200.00Unit product cost Direct materials and labor $200 $80.00 Factory overhead: Engineering $ 10 $ 3.75 Setups 40 5.00 Machine running 100 50.00 Packing 5 155 2.50 61.25Cost per unit 355 141.25 Unit margin $ 45 $ 58.75

EXHIBIT 5.6Product Profi tability Analysis under the ABC Costing System

Chapter 5 Activity-Based Costing and Management 131

Critical Questions ABC/M Tools

What do we do? Activity analysisHow much does it cost? Activity-based costingHow well do we do it? Performance measurementHow can we do it better? Benchmarking, total quality management, business process

improvement, reengineering, and value-added analysis

EXHIBIT 5.8The Role of ABC/M Tools

ABM applications use management techniques such as activity management, business pro-cess reengineering, total quality management, and performance measurement.

Strategic ABM attempts to alter the demand for activities and increase profi tability through improved activity effi ciency. Strategic ABM focuses on choosing appropriate activities for the operation, eliminating nonessential activities and selecting the most profi table customers. Strategic ABM applications use management techniques such as process design, customer profi tability analysis, and value chain analysis.

Exhibit 5.8 illustrates questions that strategic and operational ABC/ABM (ABC/M) can help to answer and the tools that are used. Some of the key tools of ABC/M are activity analy-sis, activity-based costing, performance measurement (covered in Chapters 17 and 18), and several contemporary management techniques explained in Chapter 1: benchmarking, total quality management, business process improvement, and reengineering. Another technique, value-added analysis, is explained here. We take a look now at activity analysis and value-added analysis.

Activity Analysis To be competitive a fi rm must assess each of its activities based on its need by the product or customer, its effi ciency, and its value content. A fi rm performs an activity for one of the following reasons:

It is required to meet the specifi cation of the product or service or satisfy customer demand.

It is required to sustain the organization.

It is deemed benefi cial to the fi rm.

Examples of activities required to sustain the organization are providing plant security and compliance with government regulations. Although these activities have no direct effect on the product or service or customer satisfaction, they cannot be eliminated. Examples of discretionary activities deemed benefi cial to the fi rm include a holiday party and free coffee. Exhibit 5.9 depicts an activity analysis.

Value-Added Analyses Eliminating activities that add little or no value to customers reduces resource consumption and allows the fi rm to focus on activities that increase customer satisfaction. Knowing the val-ues of activities allows employees to see how work really serves customers and which activi-ties may have little value to the ultimate customers and should be eliminated or reduced.

A high-value-added activity increases signifi cantly the value of the product or service to the customers. Removal of a high-value-added activity decreases perceptively the value of the product or service to the customer. Inserting a fl ange into a part, pouring molten metal into a mold, and preparing a fi eld for planting are examples of high-value-added activities. Installing software to protect a computer from spam is a high-value-added activity to customers annoyed by bombardments of unwanted e-mail. Designing, processing, and delivering products and services are high-value-added activities.

Exhibit 5.10 illustrates high-value-added and low-value-added activities of a television news broadcasting fi rm. For a television news broadcasting company a high-value-added activity is one that, if eliminated, would affect the accuracy and effectiveness of the newscast and decrease viewer satisfaction and ratings for that time slot. An activity that shortens deli-very from three to two days is a high-value-added activity. Activities that verify story sources

•

•

•

A high-value-added activity increases the value of the product or service to the customers.

A high-value-added activity increases the value of the product or service to the customers.

to ensure the story’s accuracy are high-value-added activities. Activities to plan newscasts so that viewers can follow transitions from one story to the next are high-value-added activities. High-value-added activities are those:

That are necessary or required to meet customer requirements or expectations.

That enhance purchased materials or components of a product.

That contribute to customer satisfaction.

That are critical steps in a business process.

That are performed to resolve or eliminate quality problems.

That are performed upon request of a satisfi ed customer.

That you would do more of, if time permitted.

•

•

•

•

•

•

•

Eliminatethe activity toreduce cost

Reduce theactivity

frequency toreduce cost

Done

Eliminatelow-value

addedactivity to

reduce cost

SelectedActivity

No

No

No

No No

NoYes

Yes

Yes

Yes YesYes

Can theactivity be

eliminated?

Areall cost

reductionopportunities

identified?

Is theactivity required

to meet the specificationof the product or service

or satisfy customerdemand?

Can thedriver

frequency bereduced?

Doesthe

activitycontain

low-valueaddedtasks?

Is theactivity required

to sustain theorganization?

EXHIBIT 5.9Example of an Activity Analysis

EXHIBIT 5.10Television News Broadcasting Firm’s High-Value-Added and Low-Value-Added Activities

A high-value-added activity is one that, if eliminated, would affect the accuracy and effectiveness of the newscast and decrease total viewers as well as ratings for that time slot.

Activities that augment accuracy • Verifi cation of story sources and acquired information.

Activities that augment effectiveness • Effi cient electronic journalism to ensure effective taped segments. • Newscast story order planned so that viewers can follow from one story to the next. • Field crew time used to access the best footage possible. • Meaningful news story writing. • Contents of the newscast planned so that viewers get the best possible package of stories.

A low-value-added activity is one that, if eliminated, would not affect the accuracy and effectiveness of the newscast. The activity contributes nothing to the quest for viewer retention and improved ratings.

Activities that generate excess • Developing stories not used in a newscast. • Assigning more than one person to develop each facet of the same news story.

Activities that augment delay (downtime) • Newscast not completed on time because of one or more ineffi cient processes. • Too many employees on a particular shift or project.

Chapter 5 Activity-Based Costing and Management 133

ABC/M applications are now common in most industries. This section illustrates some exam-ple applications in the manufacturing and service industries and within government.

ABC/M Application in Manufacturing: Industrial Air Conditioner Units AIRCO is a manufacturer of industrial air conditioning units. The units range in size and power from 5 to 20 tons. 1 Each unit has more than 200 parts, including holding tanks, elec-tronic controllers, metal sheets, cooling coils, wires, and insulation material. Almost 90% of manufacturing workers are hourly workers, and the company operates two shifts. The organization of the manufacturing process is conventional, with separate departments for purchasing, engineering, job scheduling, materials handling, shipping, accounting, and hu-man resources. AIRCO developed an ABC system to assist in the analysis of product prof-itability. Its fi rst step was to identify the resource cost pools that make up total overhead

LEARNING OBJECTIVE 5 Describe how ABC/M is used in manufacturing companies, service companies, and governmental organizations

LEARNING OBJECTIVE 5 Describe how ABC/M is used in manufacturing companies, service companies, and governmental organizations

EXHIBIT 5.11A Classifi cation of High-Value-Added and Low-Value-Added Activities.

A low-value-added activity consumes time, resources, or space, but adds little in satisfy-ing customer needs. If eliminated, customer value or satisfaction decreases inperceptively or remains unchanged. Moving parts between processes, waiting time, repairing, and rework are examples of low-value-added activities. A low-value-added activity for a television news broadcasting company is one that, if eliminated, would have little or no effect on the accu-racy and effectiveness of the newscast; the activity contributes little or nothing to the quest for viewer retention and improved ratings. Activities such as developing stories not used in a newscast or correcting prior stories are examples of low-value-added activities for a televi-sion broadcasting company. In fact, many would consider these activities as non-value-added. Inventory, transportation, waiting, and correction are examples of low-value-added activities. Other high- and low-value-added activities are illustrated in Exhibit 5.11 .

Reduction or elimination of low-value-added activities reduces cost. Low-value-added activities are those that:

Can be eliminated without affecting the form, fi t, or function of the product or service.

Begin with prefi x “re” (such as rework or returned goods).

Result in waste and add little or no value to the product or service.

Are performed due to ineffi ciencies or errors in the process stream.

Are duplicated in another department or add unnecessary steps to the business process.

Are performed to monitor quality problems.

Are performed due to a request of an unhappy or dissatisfi ed customer.

Produce an unnecessary or unwanted output.

If given the option, you would prefer to do less of.

•

•

•

•

•

•

•

•

•

A low-value-added activity consumes time, resources, or space, but adds little or does not contribute to satisfying customer needs.

A low-value-added activity consumes time, resources, or space, but adds little or does not contribute to satisfying customer needs.

1 Heather Nachtmann, and Mohammad Hani Al-Rifai, “An Application of Activity-Based Costing in the Air Conditioner Manufacturing Industry,” The Engineering Economist, 2004, 49, pp 221–236.

Activity High-Value-Added Low-Value-Added

Designing product XSetting up XWaiting XMoving XProcessing XReworking XRepairing XStoring XInspecting XDelivering product X

of $4,458,605 at the plant (Exhibit 5.12 ). The resource costs (indirect labor, computer and software, etc.) are from the fi rm’s accounting system, which collects resources costs in these 11 categories.

The next step is to identify production activities and to use resource consumption cost driv-ers to assign the resource costs to the activity cost pools. The activity cost pools are machines; data record maintenance; material handling; product changeover (setup); scheduling and pro-duction preparation; materials receiving and handling; product shipment; and customer ser-vice ( Exhibit 5.13 , column 1). The assignment of resources to activities typically uses resource consumption cost drivers. Instead of using cost drivers, AIRCO determined the estimated contribution of each resource to each activity based on managers’ and employees’ experience. For example, the resource, maintenance costs, $60,000, was assigned entirely to the activity, machines. To illustrate, the cost of the machine activity was determined from the resources as follows (other activities were obtained in a similar way):

Machine activity cost = 20 % of the computer and software costs + 100 % of energy costs + 15 % of miscellaneous expense + 100 % of maintenance expense + 100 % of depreciation expense + 12 % of offi ce and utilities expense

The machine activity cost, and the cost of other activities is shown in column 2 of Ex-hibit 5.13 . The use of estimated percentages in place of other types of resource consumption

Overhead Resource Cost

Indirect labor $2,786,900Computer and software 731,405Product transportation 319,800Energy 170,600Facility and vehicle rent 165,870Business and training travel 66,000Miscellaneous 65,480Maintenance 60,000Depreciation 48,200Advertising 40,000Offi ce and utilities 4,355 $4,458,610

EXHIBIT 5.12AIRCO Overhead Cost Resources

EXHIBIT 5.13 AIRCO Resource Consumption Cost Pools Assigned to Activities; Activity Cost Drivers, and Activity-Based Rates

Machines $ 435,425 Number of machine hours 73,872 $ 5.89Data record maintenance 132,596 Number of products lines 14 9,471Materials handling 1,560,027 Number of products 16,872 92.46Production changeover 723,337 Setup time (hours) 72 10,046 (setup)Scheduling and production 24,876 Number of production runs 2,788 8.92 preparationMaterial receiving and 877,106 Number of receipts 2,859 306 handlingProduct shipment 561,013 Distance (miles) 13,784,015 .041Customer service 144,230 Number of customer contacts 2,533 56.94 Total $4,458,610

EXHIBIT 5.15 AIRCO: Overhead Allocation and Product Profi tability under Volume-Based Costing

cost drivers is a practical and convenient approach that is often used in implementing ABC costing.

The next step in ABC is to identify activity consumption cost drivers, to identify the total amounts for these cost drivers, and then to determine the ABC-based application rate. This is shown in Exhibit 5.13 , columns 3, 4, and 5, respectively. Thus, the cost of machine time is assigned to each of the products based on machine hours used by that product times the rate of $5.89 per machine hour ($5.89 = $435,425/73,872). This is done in the same manner for the other activities. The determination of ABC cost and profi tability analysis for AIRCO’s key product lines is the fi nal step and is shown in Exhibit 5.14 . Note that this analysis shows that the 5-ton, 6-ton and 12.5-ton products are not profi table.

The ABC analysis can be compared to the volume-based approach that AIRCO used prior to ABC. The volume-based overhead costs were assigned to products based on a rate of $12.02 per direct labor hour. The results are shown in Exhibit 5.15 . Note that the ABC and volume-based methods show signifi cantly different results for some of the products, particularly the 6-ton and 12.5-ton models. While the detailed calculations of the ABC costs for these products is not shown, the company reports that the 12.5-ton model required signifi cantly more raw ma-terials receipts (the cost driver for material receiving and handling) than other products, and it also required more setup time and customer service contacts. Thus, the ABC costs for the 12.5-ton model are signifi cantly higher than for volume-based costs. Similarly, the 6-ton prod-uct has higher costs under ABC because of its relatively high use of setup time and customer service contact. The ABC information provides the company a useful basis for becoming more competitive, for example, by reconsidering the pricing of certain products and looking for ways to increase effi ciency in the use of its activities.

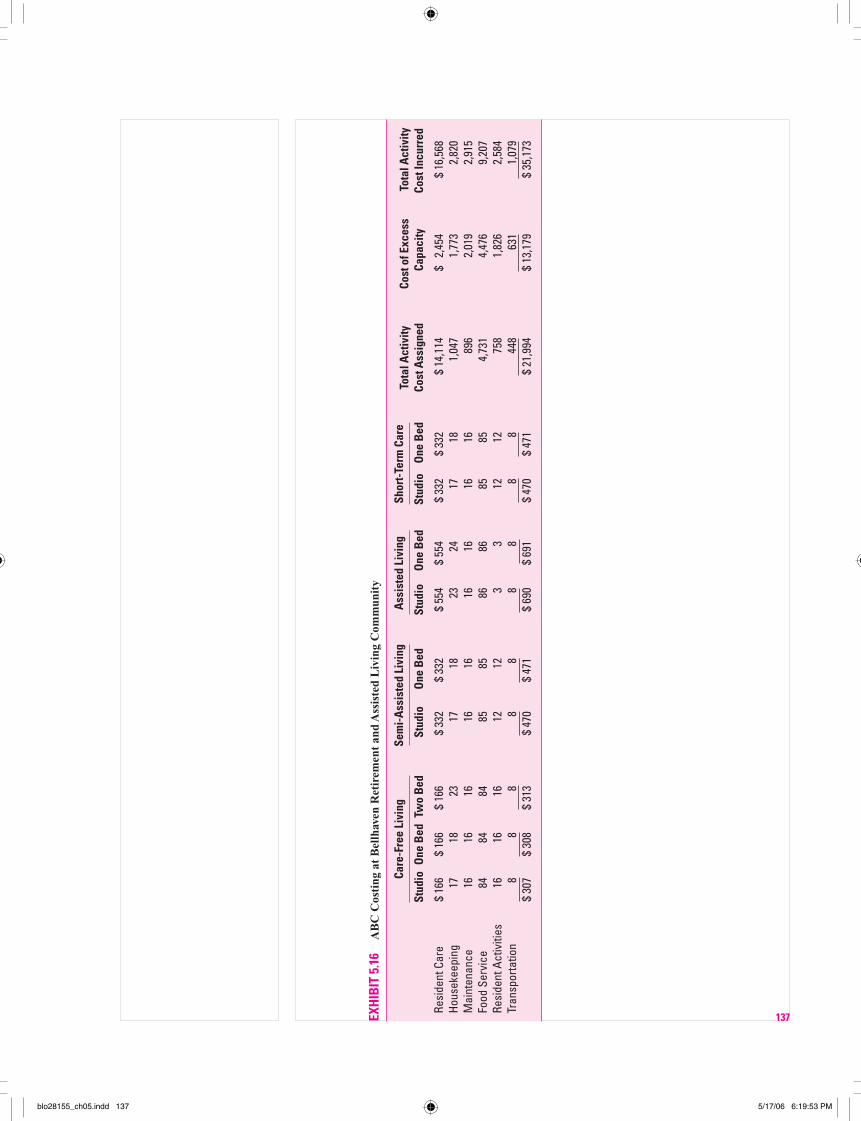

ABC/M Application in the Service Industry: A Retirement and Assisted Living Community The following is based on an actual 70-unit retirement and assisted living community, which we will call Bellhaven Homes, Inc. 2 Bellhaven has three levels of resident care: care-free

2 Sidney J. Baxendale, Mahesh Gupta, and P. S. Raju, “Profi t Enhancement Using an ABC Model,” Management Accounting Quarterly, Winter 2005, pp. 11–21.

living, semi-assisted living, assisted living, and short-term care. Each is offered in a studio or one bedroom fl oor plan, except care-free living, which is also offered in a two-bedroom fl oor plan. These nine different care-level/fl oor-plan combinations are priced differently and are re-garded as the cost objects at Bellhaven. There are currently 56 residents at Bellhaven, spread across the nine cost objects. The services at Bellhaven include resident care, housekeeping, maintenance of grounds and facility, food service, resident activities, and transportation. Each of these six services are the activities used by Bellhaven in developing an ABC model to deter-mine the cost and profi tability of each of its nine cost objects. The cost drivers for each activity are the number of hours worked by employees in each of these activities. The ABC application rates are then determined from the hours available in each of the service units, and the ABC costs for each cost object are calculated. Exhibit 5.16 illustrates the per resident costs within each of the nine cost objects. The ABC analysis provides Bellhaven useful information for pric-ing its services and for identifying activities where costs can be reduced and/or value added.

A special feature of the Bellhaven analysis is the calculation of the cost of unused capacity. Since Bellhaven maintains staff suffi cient to cover all 70 units in the facility, it is important to track the costs of underutilization. Bellhaven has room for 14 more residents. This means that the application rates are based on 70-unit capacity and not actual usage, as is sometimes the case in ABC. When rates are based on capacity, management is able to determine the additional information about the cost of unused capacity.

ABC/M Applications in Government ABC/M is used widely in government. The U.S. Postal Service example that introduced this chapter is one good example. Another example is the U.S. Patent and Trademark Offi ce (PTO) which uses ABC to better understand its cost structure. As the volume of patent requests has increased substantially, and since the PTO is not taxpayer supported but relies on user fees, the determination of accurate costs and the setting of appropriate user fees for its different services is critical. The ABC model at the PTO used 29 activities and the cost objects included utility patents, design patents, plant patents, reissues, reexaminations, trademarks, and ap-peals. One fi nding of the ABC implementation was that the cost of trademark processing was higher than expected. 3

3 For additional examples: Gary Cokins, Activity-Based Cost Management in Government, Management Concepts, Inc., 2001.

REAL-WORLD FOCUS Distorted Medicare Reimbursement with Inappropriate Cost Drivers

Hospitals must complete a Medicare cost report each year to be eligi-ble for government reimbursement for services rendered to Medicare patients. Government uses this cost information to set amounts for various Medicare reimbursement parameters. Hospitals often use the same cost information as the basis for determining the charges for privately insured patients. For inpatient care costs, Medicare requires that all operating costs pertaining to patient care be allocated to pa-tients based only on the number of days a patient spends in the hos-pital (patient-days). Thus, Medicare cost reporting does not explicitly consider the possibility of multiple cost drivers.

Huang and Kirby noted at least two cost drivers for patient care costs: (1) the number of patient-days and (2) the number of patients admitted. Patient-day costs include costs of meals, laundry, and basic nursing care. Admission costs include costs for taking patients’ his-tory upon admission, preparing patients for surgery, intensive care immediately following surgery, preparing rooms for new patients, and handling medical coding and billing. The fi rst cost driver, the number of patient-days, is a unit-level cost driver while the second cost driver is likely a batch-level cost driver.

Using publicly available data, Huang and Kirby compared the results of current Medicare reimbursement procedures that use a

single volume-based, unit-level cost driver (patient-days), with the results that would be obtained if Medicare reimbursements were based on two cost drivers: a unit-level cost driver (patient-days) and a batch-level cost driver (number of admissions). Their studyresults suggest that Medicare is potentially overcharged by between $66 million and $1.98 billion per year for hospital patient care! The main reason is that Medicare patients tend to be older and have a much longer average length of hospitalization than private insur-ance patients do. Because Medicare reimbursements consider only patientdays, Medicare is charged for a disproportionately large share of admitted patients.

Moreover, Medicare reimbursement for a given medical proce-dure is based on a formula developed by the Health Care Financ-ing Administration (HCFA) which relies on physician time and the complexity of the procedure. Since some of the costs of any given procedure may not be related to physician time and/or the complex-ity rating, the Medicare formula will not always accurately refl ect incurred costs.

Source: Yuchang Huang and Alison L. Kirby, “Distorted Medicare Reimburse-ments: The Effect of Cost Accounting Choices,” Journal of Management Accounting Research, Fall 1994, pp. 128–43.

Other examples include the Internal Revenue Service (IRS), which uses ABC/M to calcu-late the costs of processing each of its different types of tax returns, and the U.S. Army, which uses ABC in the management of the delivery of medical care and the maintenance of military equipment, among other applications.

The U.S. federal government encourages the use of ABC within its various units. In 1990, three offi cials responsible for federal fi nancial reporting established the Federal Accounting Standards Advisory Board (FASAB) as a federal advisory committee ( www.fasab.gov ). The offi cials were the Secretary of the Treasury, the Director of the Offi ce of Management and Budget, and the Comptroller General of the United States. They created FASAB to develop accounting standards and principles for the United States Government. FASAB Standard Num-ber 4, “Managerial Cost Accounting Concepts and Standards for the Federal Government, ” explains the advantages of ABC for use in governmental units.

Customer Profi tability Analysis

How is customer service doing? Bezos isn’t interested in a qualitative answer. He wants to

know average customer contacts per hour, average time per contact, the breakdown of e-mail

versus telephone, and the total cost to the company of each.

Interview with Jeff Bezos , CEO of Amazon.com, Fortune , May 26, 2003, p. 64.

ABC/M is best known for its application in computing product costs, but many fi rms fi nd that it is also very useful in determining the cost of serving customers and as a basis for evaluating the profi tability of a specifi c customer or of a selected group of customers. Why is this impor-tant? Most managers agree that 80% of their profi ts come from the top 20% of their customers, and most important, the bottom 20% of their customers are unprofi table! For example, to bet-ter compete with Wal-Mart, Best Buy works hard to attract profi table customers (it calls them angels ) and equally hard to discourage the unprofi table customers (the devils ), those that are price shopping and looking for discounts and promotions, and comparing prices to Wal-Mart. This strategy involves improved service and fewer discount/promotion offers. Best Buy stud-ies demographic and sales data for each store location to identify angels and devils. Similarly, the large food distributor, CONCO, studies its customer base (mostly restaurants) to identify profi table and unprofi table customers. CONCO found that certain food products and smaller customers tended to be unprofi table. 4

Customer profi tability analysis identifi es customer service activities and cost drivers and determines profi tability of each customer or group of customers. Here, customer service in-cludes all activities to complete the sale and satisfy the customer, including advertising, sales calls, delivery, billing, collections, service calls, inquiries, and other forms of customer ser-vice. Customer profi tability analysis allows managers to:

Identify most profi table customers.

Manage each customer’s costs-to-serve to a lower level.

Establish a surcharge for or repricing expensive costs-to-serve activities.

Reduce services for high cost-to-serve customers.

Introduce new products and services.

Discontinue products, services, or customers.

Improve the process of customer service.

Shift the customer’s purchase mix toward higher-margin products and service lines.

Offer discounts to gain more volume with low costs-to-serve customers.

Select customer mix—What types of customer should we market to? What types should we not market to?

Choose types of after-sale services to provide.

•

•

•

•

•

•

•

•

•

•

•

Customer profi tability analysis identifi es customer service activities, cost drivers, and the profi tability of individual customers or groups of customers.

Customer profi tability analysis identifi es customer service activities, cost drivers, and the profi tability of individual customers or groups of customers.

4 Stephen Schulist, “Using ABC to Manage and Improve at CONCO Foods,” The Journal of Corporate Accounting & Finance, March/April 2004, pp. 29–34; Gary McWilliams, “Analyzing Customers, Best Buy Decides Not All Are Welcome,” The Wall Street Journal, November 8, 2004, p. 1.

b lo 2 8 1 5 5 _ c h 0 5 . in d d 1 3 8blo28155_ch05.indd –1385 / 1 7 / 0 6 6 : 1 9 : 5 3 P M5/17/06 –6:19:53 PM

Chapter 5 Activity-Based Costing and Management 139

A good understanding of the profi tability of a fi rm’s current and potential customers can help fi rms to improve overall profi ts and to become more competitive. This begins with an analysis of the cost to serve the customer.

Customer Cost Analysis Not all customers require similar activities either before or after the sales. Examples of customer-specifi c activities include:

Order processing costs.

Billing, collection, and payment processing costs.

Accounts receivable and carrying costs.

Customer service costs.

Return or allowance processing costs.

Restocking costs.

Selling and marketing costs.

Customer cost analysis identifi es activities and cost drivers to service customers before and after sales, not including product costs. Traditionally these costs are hidden in the cus-tomer support, marketing, and sales function. ABC/M can help managers to grasp activities and their costs to serve customers.

Different activities often have different cost drivers. Based on the activities and cost drivers involved in services performed to acquire and complete a transaction, customer costs can be classifi ed into the following categories:

Customer unit-level cost —resources consumed for each unit sold to a customer. Examples include sales commissions based on the number of units sold or sales dollars, shipping cost when the freight charge is based on the number of units shipped, and cost of restocking each of the returned units.

Customer batch-level cost —resources consumed for each sales transaction. Examples in-clude order-processing costs, invoicing costs, and recording of sales returns or allowances every time a return or allowance is granted.

Customer-sustaining cost —resources consumed to service a customer regardless of the number of units or batches sold. Examples are salespersons’ travel costs to visit customers, monthly statement processing costs, and collection costs for late payments.

Distribution-channel cost —resources consumed in each distribution channel the fi rm uses to service customers. Examples are operating costs of regional warehouses that serve major customers and centralized distribution centers that serve small retail outlets.

Sales-sustaining cost —resources consumed to sustain sales and service activities that can-not be traced to an individual unit, batch, customer, or distribution channel. Examples are general corporate expenditures for sales activities, and salary, fringe benefi ts, and bonus of the general sales manager.

Exhibit 5.17 reports customer-related activities, cost drivers and their rates, and the cost category of each of the activities of Winsome Offi ce Supply. These activities are based on the results of a careful study of the fi rm’s selling, administrative, and general expenditures, as well as customer transactions for the last three years. Exhibit 5.18 reports the detailed customer-related activities that Winsome experienced for the sales to the fi rm’s three major customers GereCo, HomeServ Inc, and Advance Tek.

Both customer activity costs, cost categories, and their cost drivers illustrated in Exhibit 5.17 and the detailed customer-related activities reported in Exhibit 5.18 provide the basis for analyzing customer costs. Exhibit 5.19 reports customer cost analyses for Winsome’s three customers.

As illustrated in Exhibit 5.18 and 19 , the costs to service customers often differ because they do not require the same amount of services. These three customers purchased approxi-mately equal amounts from Winsome. The costs to serve these customers, however, ranged from $1,555 to $10,795.

•

•

•

•

•

•

•

•

•

•

•

•

LEARNING OBJECTIVE 6 Use an activity-based approach to analyze customer profi tability

LEARNING OBJECTIVE 6 Use an activity-based approach to analyze customer profi tability

Customer cost analysis identifi es activities and cost drivers to service customers.

Customer cost analysis identifi es activities and cost drivers to service customers.

Customer Profi tability Analysis Customer profi tability analysis combines customer revenues and customer cost analyses to assess customer profi tability and helps identify actions to improve customer profi tability. Exhibit 5.20 illustrates customer profi tability analysis for Winsome.

The customer profi tability analysis shows that HomeServ is the most profi table among Winsome‘s three major customers, even though HomeServ had the lowest amount of

EXHIBIT 5.17Customer-Related Activity, Cost Driver, Cost Rate, and Cost Category

Activity Cost Driver and Rate Cost Category

Order taking $30 per order Customer batch-levelOrder processing $20 per order, and Customer batch-level $1 per item Customer unit-levelDelivery $100 per trip, and Customer batch-level $1 per mile Customer batch-levelExpedited order taking, $800 per order Customer batch-level processing, and delivery (additional costs) Customer visit $200 per visit Customer sustainingMonthly billing: First statement $5 per statement Customer sustaining Subsequent reminder $25 per notice Customer sustainingSales returns $100 per occurrence Customer batch-levelRestocking $5 per item returned Customer unit-levelSales offi ce Salaries and fringe benefi ts $100,000 per month Sales sustaining Offi ce expenses $50,000 per month Sales sustaining

EXHIBIT 5.18Customer-Related Activity for Selected Customers Winsome Offi ce Supply

GereCo. HomeServ Inc. Advance Tek

Net sales $463,917 $477,600 $472,576Number of orders 2 20 80Average number of items per order 400 38 8Delivery miles 10 15 20Number of expedited orders 0 0 5Number of visits by salesperson 1 2 5Sales returns Number of requests 2 1 10 Average units per return 3 4 2

EXHIBIT 5.19Customer Cost Analysis, Winsome Offi ce Supply

purchases from Winsome. The analysis also shows that although Advance Tek made the high-est total purchases of the three, it yields the lowest net customer profi t.

The reasons that GereCo. is not as profi table as HomeServ relate to sales activities. Win-some granted GereCo. much more favorable sales terms than the terms granted to HomeServ. GereCo. also had a high amount of sales returns and allowances; it returned twice as often as HomeServ did.

Discounts and sales returns are contributing factors for the low profi tability of Advance Tek. Although Advance Tek had the highest total sales, it generated the lowest profi t of the three customers. Winsome should be concerned about Advance Tek’s high returns and its fre-quency of expediting orders. The high returns could be a result of the customer’s dissatisfac-tion with Winsome’s products. Winsome needs to look into the reason for the high returns before losing the customer to competition. Late payments also add cost to serve Advance Tek; they might indicate Advance Tek’s dissatisfaction with Winsome’s sales and services or tight-ness of Advance Tek’s fi nancial condition.

Customer Value Assessment Customer profi tability analysis provides valuable information to the assessment of customervalue. In addition, fi rms must weigh other relevant factors before determining the action appropriate for each customer. The following are among these relevant factors:

Growth potential of the customer, the customer’s industry, and its cross-selling potential.

Possible reactions of the customer to changes in sales terms or services.

•

•

Cost Management in Action CUSTOMER PROFITABILITY: IS IT BETTER FOR WEB CUSTOMERS?

An important part of customer profi tability is the cost to acquire a new customer. Bain and Company, a consulting fi rm, estimated that the cost of obtaining a new customer in the consumer electronics industry needs more than four years of business from each new customer to break even,

but more than half of the new customers will defect before the four-year breakeven point. The numbers are similar for the apparel industry. Many fi rms are now trying to acquire new customers through the Web. What would be the effect of the Web acquisition on profi tability?

EXHIBIT 5.20Customer Profi tability Analysis, Winsome Offi ce Supply

REAL-WORLD FOCUS ABC/M: Which Companies Have Success?

The Consortium for Advanced Manufacturing International (CAM-I) and the American Productivity and Quality Center (APQC) recently collaborated in the survey of 166 manufacturing and service fi rms to assess the implementation of ABC/M in these fi rms. Sixty-eight per-cent of the respondents were in manufacturing and 25% in service companies. The results showed that the majority of senior managers reported “very successful” implementations of the ABC/M system, while department managers were somewhat evenly split between “very successful” and “moderately successful.” Line personnel tend-ed to vote “moderately successful.” So, the higher the respondents were in the organization, the more they perceived benefi ts from use of the ABC/M system.

Interviews with selected respondents and further data analysis showed that the three most common characteristics of successful

systems were: (1) a high level of top management support and com-mitment; (2) technical competence of the implementation team; and (3) effective change management, that is, companies driven by com-petitive pressures to strive to better understand their internal capa-bilities and external competition. Some of the responding companies made strategic changes, including changes in the supply chain and changes in target customers. These results are similar to those re-ported in prior studies of ABC/M implementation.