1 Traditional Costing Systems In Traditional Costing Systems • Allocate overhead using a single predetermined rate. • Job order costing: direct labor cost is assumed to be the relevant activity base. • The assumption was satisfactory when direct labor was a major portion of total manufacturing costs. • Wide acceptance of a high correlation between direct labor and overhead costs. • In traditional cost accounting, only manufacturing cost are assigned to products • Administrative expenses are treated as period expenses and are not assigned to products.

Transcript

1

Traditional Costing Systems

In Traditional Costing Systems

• Allocate overhead using a single predetermined rate.

• Job order costing: direct labor cost is assumed to be the

relevant activity base.

• The assumption was satisfactory when direct labor was a

major portion of total manufacturing costs.

• Wide acceptance of a high correlation between direct labor

and overhead costs.

• In traditional cost accounting, only manufacturing cost are

assigned to products

• Administrative expenses are treated as period expenses

and are not assigned to products.

2

The Need for a New Approach

Tremendous change in manufacturing and service

industries.

Decrease in the amount of direct labor used.

Significant increase in total overhead costs.

Inappropriate to use plant-wide predetermined overhead

rates when a lack of correlation exists.

Complex manufacturing processes may require multiple

allocation bases; this approach is called Activity-Based

Costing (ABC).

3

Activity-Based Costing System

In activity-based costing (ABC), products are assigned all

of the overhead cost.

Activity-based costing (ABC) refines a costing system by

identifying individual activities as the fundamental cost

objects.

An activity is an event, task, or unit of work with a

specified purpose—for example, designing products, setting

up machines, operating machines, and distributing products.

* Activity Cost Pool :the overhead cost attributed to a

distinct type of activity For example: ordering materials or

setting up machines

* Cost Driver: any factor or activity that has a direct

cause-effect relationship with the resources consumed.

*

ABC allocates overhead costs in two stages

Stage 1:Overhead costs are allocated to activity cost pools.

Stage 2:The overhead costs allocated to the cost pools is

assigned to products using cost drivers.

4

Guidelines for refining costing system

1: Identify the Products that are the Chosen Cost Objects.

2: Identify the Direct Costs of the Products.

3: Select the Activities and Cost-Allocation Bases to Use for

Allocating Indirect Costs to the Products.

Steps for implementing Activity-Based

Costing ABC System

Step 1: Identify and Classify Activities and Allocate Overhead

to activity Cost Pool.

Step 2: Identify Cost Drivers.

Step 3: Compute activity-based Overhead Rates.

Step 4: Assign overhead cost to Products (cost objects).

5

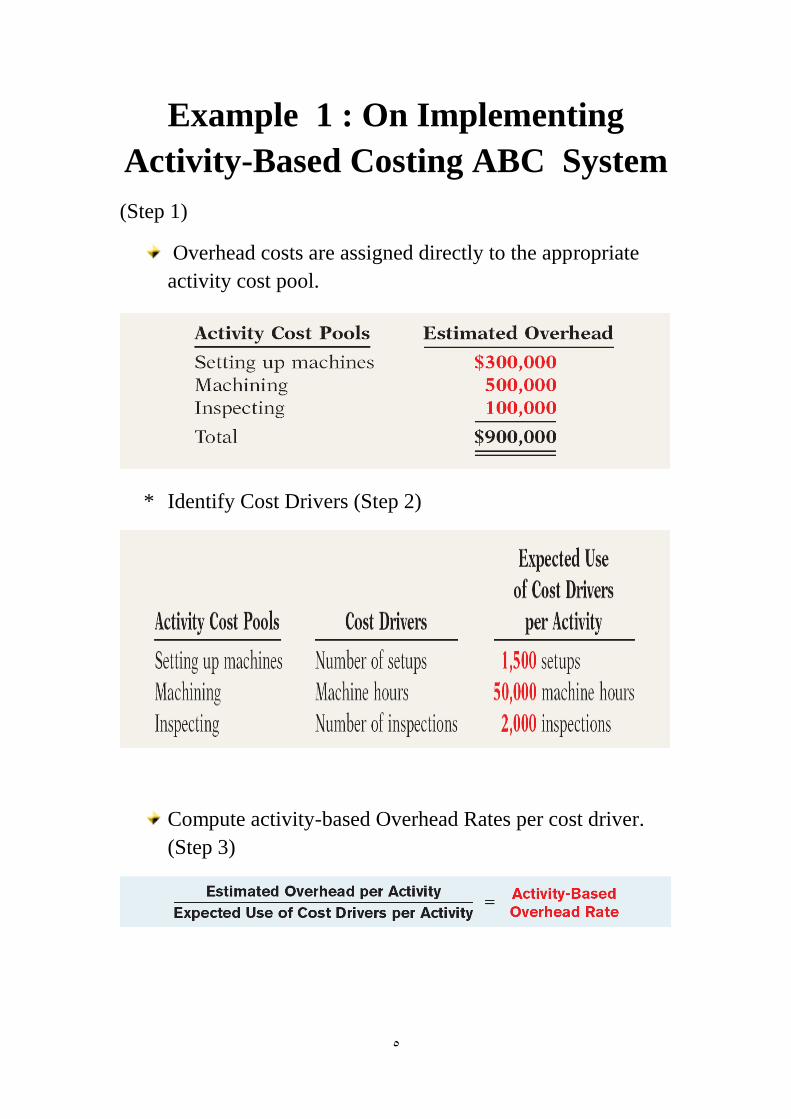

Example 1 : On Implementing

Activity-Based Costing ABC System

(Step 1)

Overhead costs are assigned directly to the appropriate

activity cost pool.

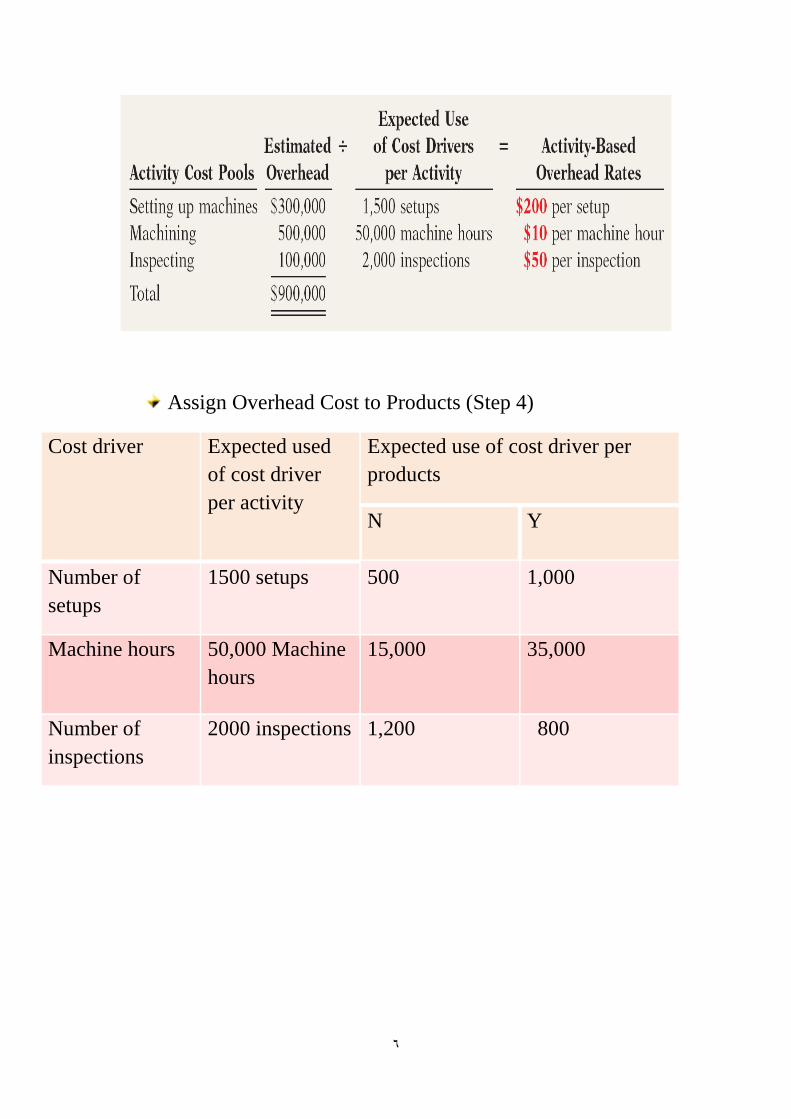

* Identify Cost Drivers (Step 2)

Compute activity-based Overhead Rates per cost driver.

(Step 3)

6

Assign Overhead Cost to Products (Step 4)

Expected use of cost driver per

products

Expected used

of cost driver

per activity

Cost driver

Y N

1,000 500 1500 setups Number of

setups

35,000 15,000 50,000 Machine

hours

Machine hours

800 1,200 2000 inspections Number of

inspections

7

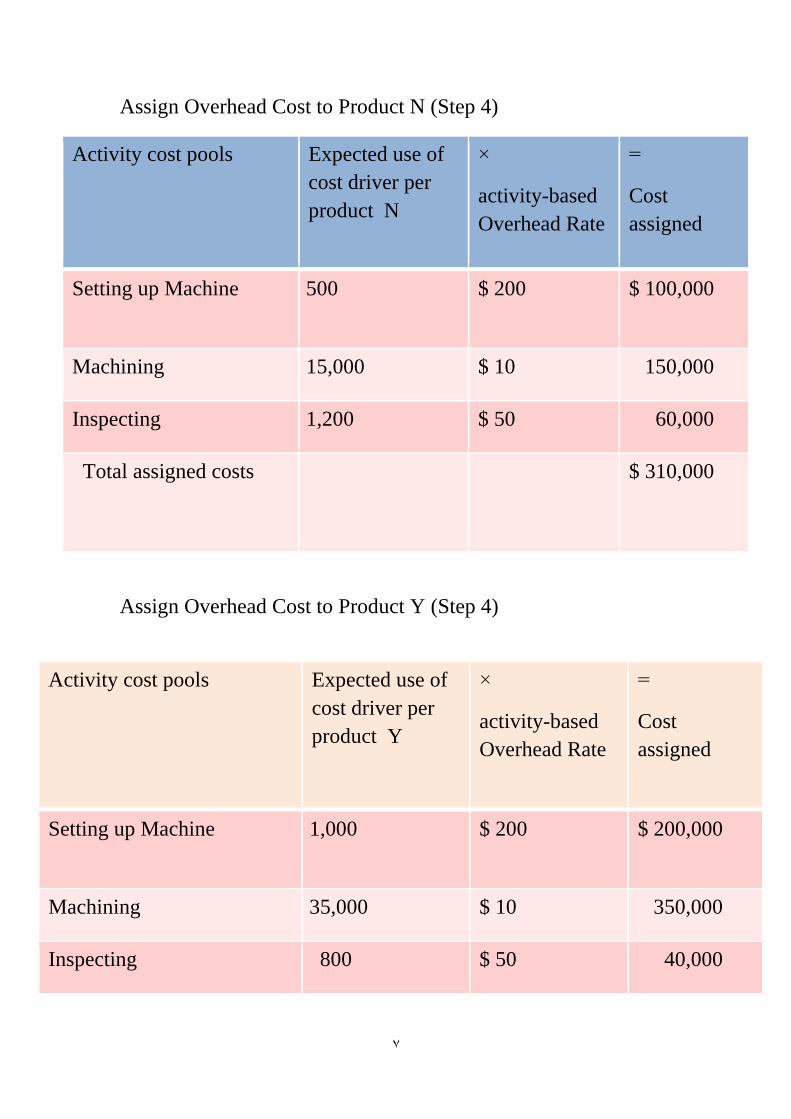

Assign Overhead Cost to Product N (Step 4)

=

Cost

assigned

×

activity-based

Overhead Rate

Expected use of

cost driver per

product N

Activity cost pools

$ 100,000 $ 200 500 Setting up Machine

150,000 $ 10 15,000 Machining

60,000 $ 50 1,200 Inspecting

$ 310,000 Total assigned costs

Assign Overhead Cost to Product Y (Step 4)

=

Cost

assigned

×

activity-based

Overhead Rate

Expected use of

cost driver per

product Y

Activity cost pools

$ 200,000 $ 200 1,000 Setting up Machine

350,000 $ 10 35,000 Machining

40,000 $ 50 800 Inspecting

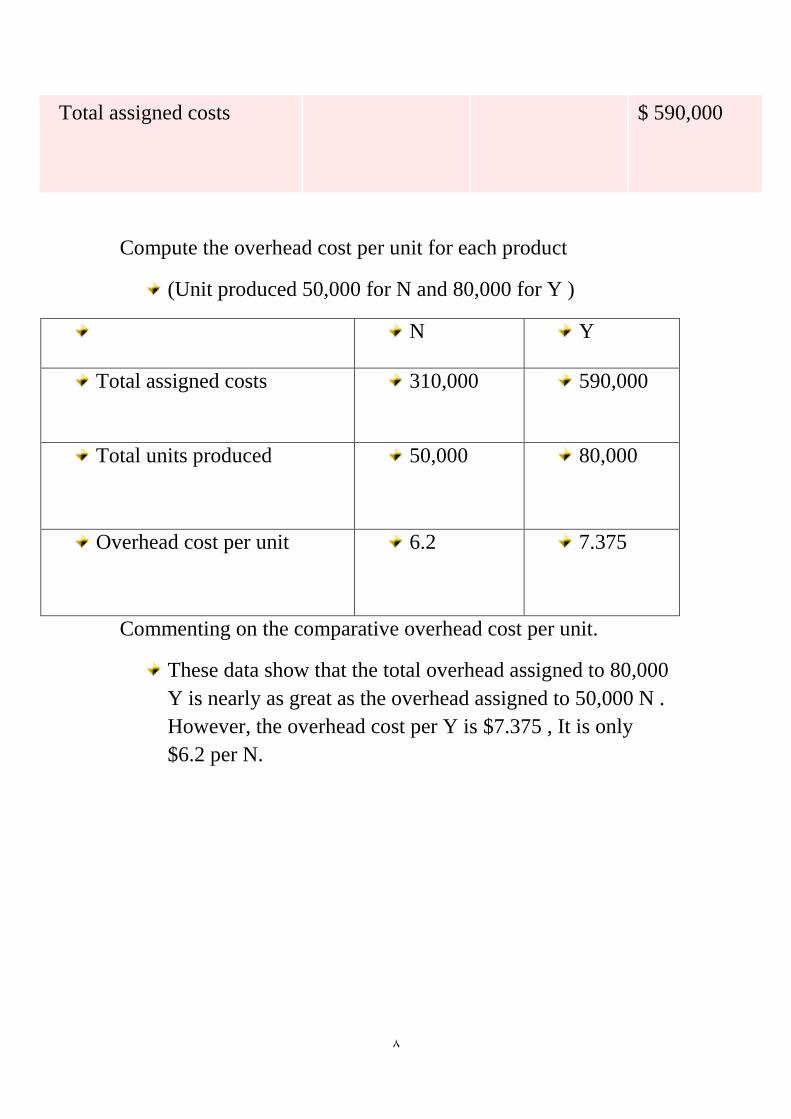

8

Compute the overhead cost per unit for each product

(Unit produced 50,000 for N and 80,000 for Y )

Y N

590,000 310,000 Total assigned costs

80,000 50,000 Total units produced

7.375 6.2 Overhead cost per unit

Commenting on the comparative overhead cost per unit.

These data show that the total overhead assigned to 80,000

Y is nearly as great as the overhead assigned to 50,000 N .

However, the overhead cost per Y is $7.375 , It is only

$6.2 per N.

$ 590,000 Total assigned costs

9

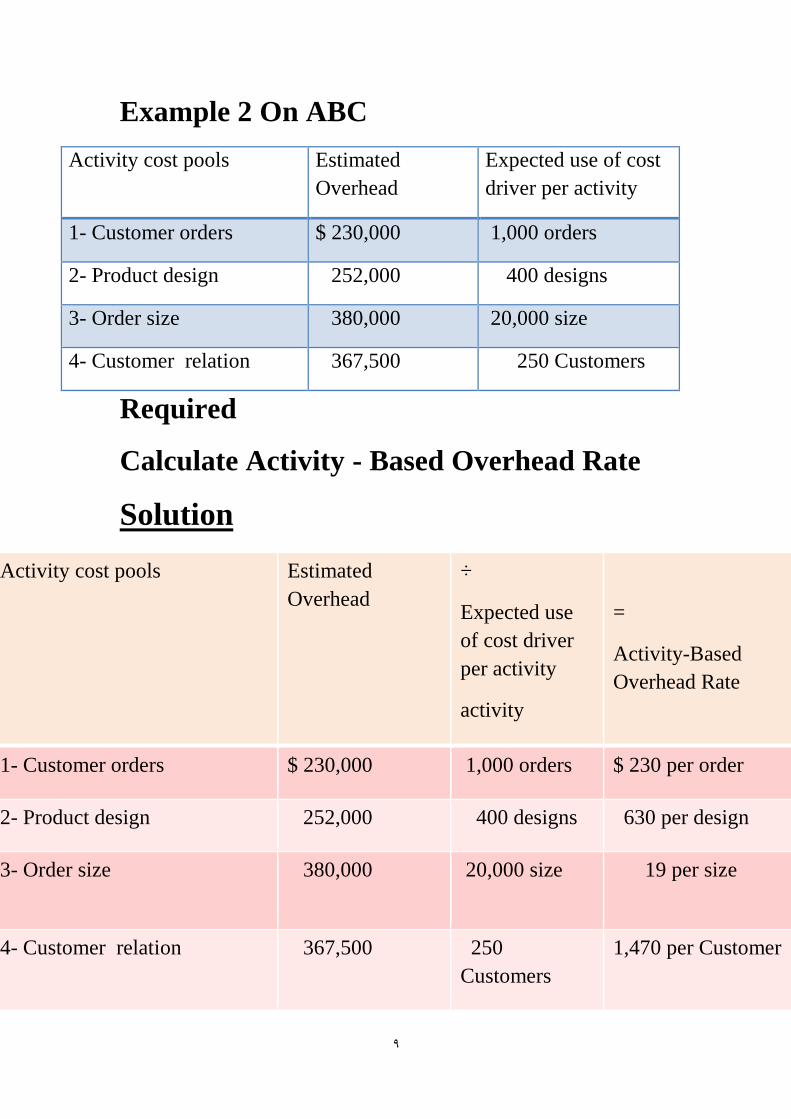

Example 2 On ABC

Expected use of cost

driver per activity

Estimated

Overhead

Activity cost pools

1,000 orders $ 230,000 1- Customer orders

400 designs 252,000 2- Product design

20,000 size 380,000 3- Order size

250 Customers 367,500 4- Customer relation

Required

Calculate Activity - Based Overhead Rate

Solution

=

Activity-Based

Overhead Rate

÷

Expected use

of cost driver

per activity

activity

Estimated

Overhead

Activity cost pools

$ 230 per order 1,000 orders $ 230,000 1- Customer orders

630 per design 400 designs 252,000 2- Product design

19 per size 20,000 size 380,000 3- Order size

1,470 per Customer 250

Customers

367,500 4- Customer relation

10

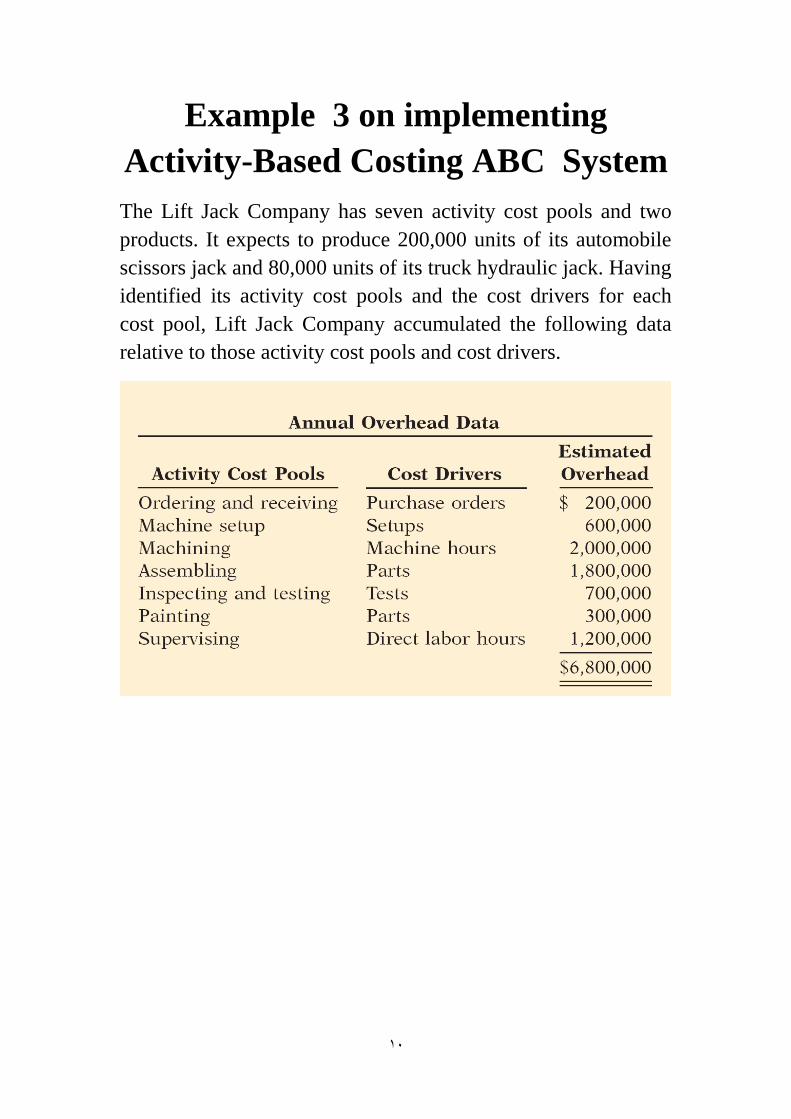

Example 3 on implementing

Activity-Based Costing ABC System

The Lift Jack Company has seven activity cost pools and two

products. It expects to produce 200,000 units of its automobile

scissors jack and 80,000 units of its truck hydraulic jack. Having

identified its activity cost pools and the cost drivers for each

cost pool, Lift Jack Company accumulated the following data

relative to those activity cost pools and cost drivers.

11

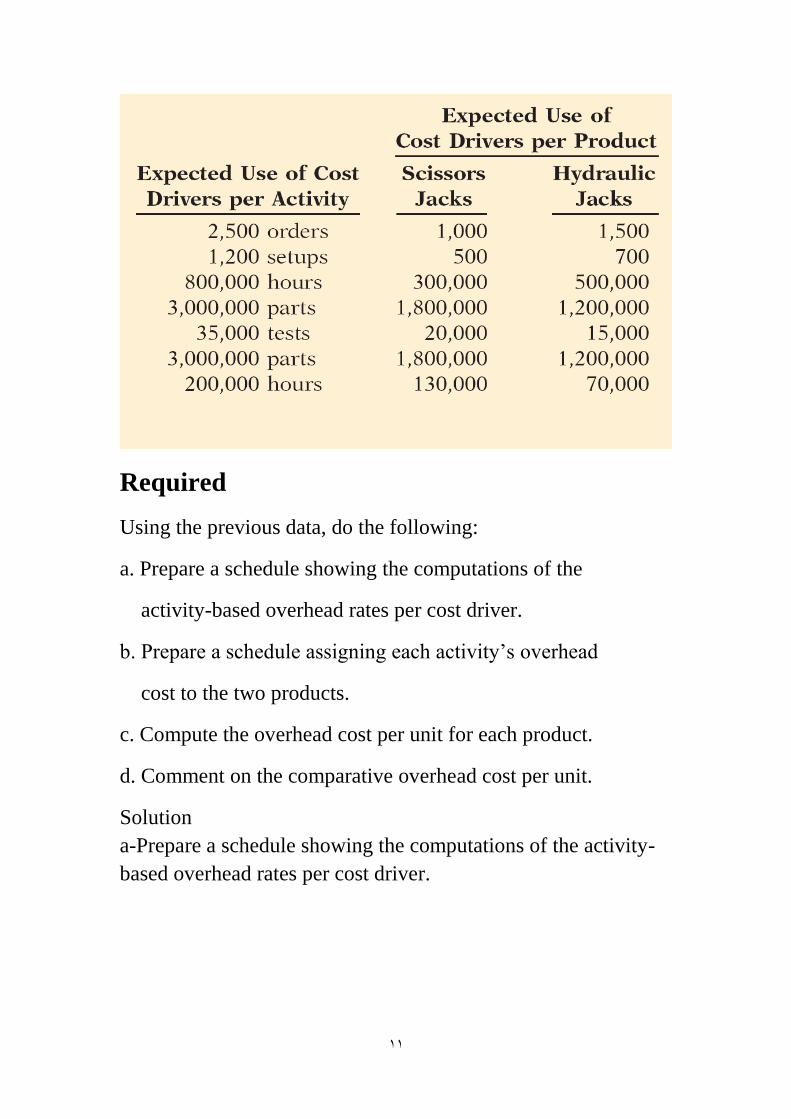

Required

Using the previous data, do the following:

a. Prepare a schedule showing the computations of the

activity-based overhead rates per cost driver.

b. Prepare a schedule assigning each activity’s overhead

cost to the two products.

c. Compute the overhead cost per unit for each product.

d. Comment on the comparative overhead cost per unit.

Solution

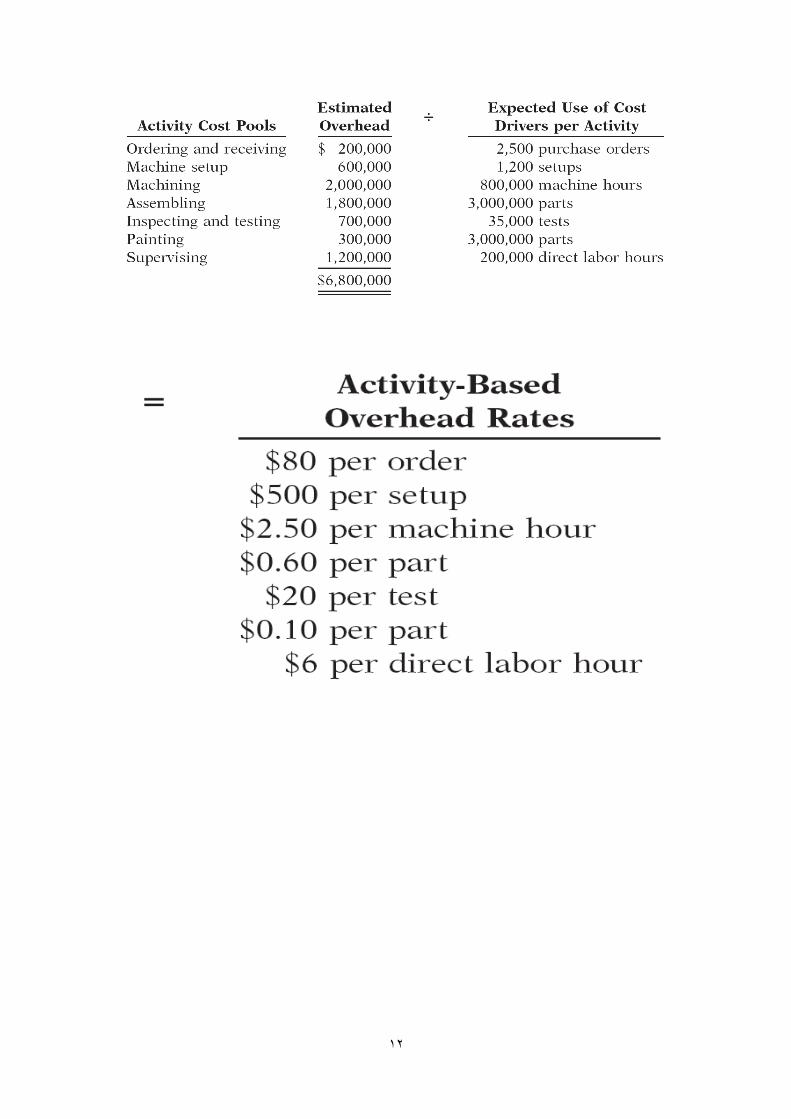

a-Prepare a schedule showing the computations of the activity-

based overhead rates per cost driver.

12

13

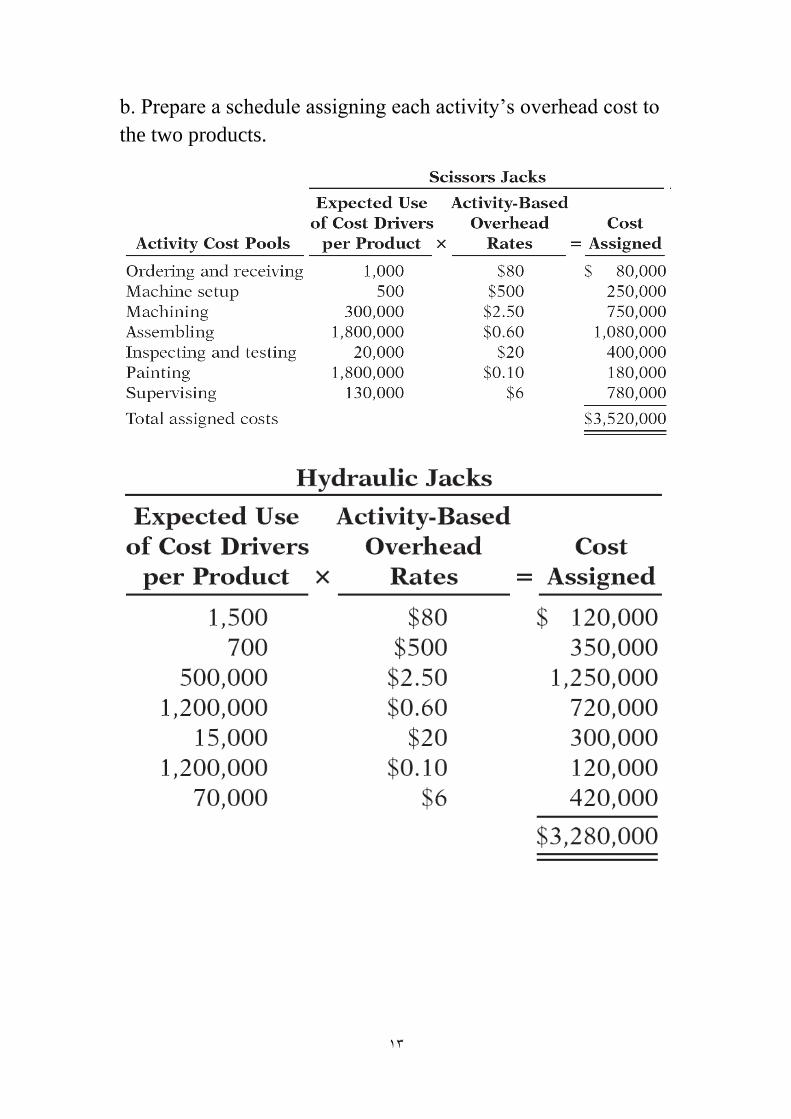

b. Prepare a schedule assigning each activity’s overhead cost to

the two products.

14

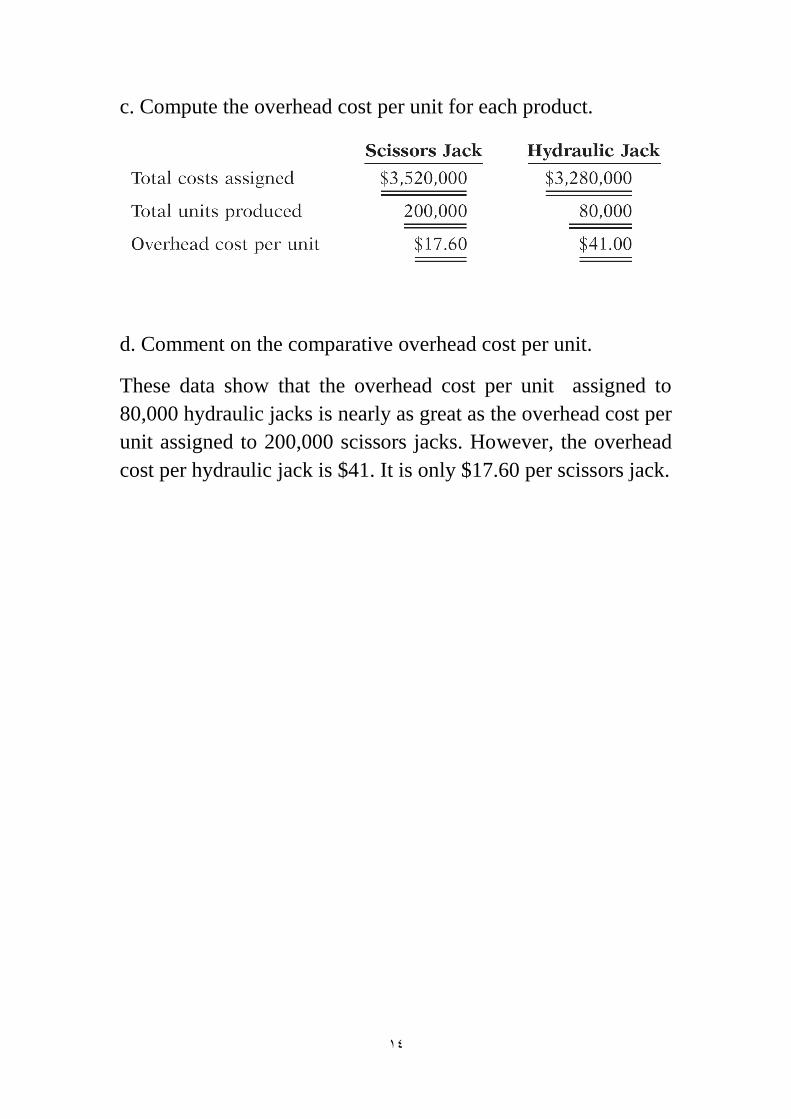

c. Compute the overhead cost per unit for each product.

d. Comment on the comparative overhead cost per unit.

These data show that the overhead cost per unit assigned to

80,000 hydraulic jacks is nearly as great as the overhead cost per

unit assigned to 200,000 scissors jacks. However, the overhead

cost per hydraulic jack is $41. It is only $17.60 per scissors jack.